|

|

THE TAX APPEALS TRIBUNAL (APPEALS TO THE HIGH COURT) RULES

ARRANGEMENT OF RULES

| 3. |

Time for filing of memorandum of appeal

|

| 4. |

Extension of time for filing memorandum of appeal

|

| 6. |

Filing of memorandum of appeal and other documents

|

| 8. |

Filing of statement of facts

|

| 9. |

Response and extension of time

|

| 10. |

Notice to parties to appear for hearing

|

| 11. |

Reasons for dismissing appeal

|

| 12. |

Reinstatement of appeal

|

| 14. |

Limitations on grounds to rely on

|

| 15. |

Admission of other evidence

|

| 16. |

Admissibility of evidence

|

| 17. |

Ancillary applications

|

| 18. |

Where a court decrees does not specify tax payable

|

| 20. |

Civil procedures to apply

|

| 21. |

Appeal to the Court of appeal

|

THE TAX APPEALS TRIBUNAL (APPEALS TO THE HIGH COURT) RULES, 2015

| 1. |

Citation

These Rules may be cited as the Tax Appeals Tribunal (Appeals to the High Court) Rules, 2015.

|

| 2. |

Interpretation

In these Rules, unless the context otherwise requires—

"address for service" means a place of residence or a place of business or last known address;

"appeal” means an appeal to the High Court under section 32 of the Act;

"Registrar" means the Registrar of the High Court.

|

| 3. |

Time for filing of memorandum of appeal

The appellant shall, within thirty days, after the date of service of a notice of appeal under section 32(1), file a memorandum of appeal with the Registrar and serve a copy on the respondent.

|

| 4. |

Extension of time for filing memorandum of appeal

The Court may extend the time specified in rule 3 if the Court is satisfied that, owing to absence from Kenya, sickness, or other reasonable cause, the appellant was unable to file the memorandum of appeal within that period and that there has been no unreasonable delay on the part of the appellant.

|

| 5. |

Memorandum of appeal

A memorandum of appeal shall—

| (a) |

be signed by the appellant;

|

| (b) |

contain an address of service of the appellant;

|

| (c) |

set out concisely under consecutively numbered distinct heads, the grounds of appeal without any arguments or narrative;

|

| (d) |

contain an index of all documents supporting the appeal with number of pages at which they appear; and

|

| (e) |

accompanied by a copy of the decision of the Tribunal and the notice of appeal.

|

|

| 6. |

Filing of memorandum of appeal and other documents

| (1) |

After the memorandum of appeal and the supporting documents have been filed, the Registrar shall stamp the memorandum of appeal and the documents filed, and number and enter the Appeal, as a Tax Appeal, in the register of tax appeals.

|

| (2) |

Upon entry of an appeal in the register of tax appeals, the Registrar shall ensure that, in respect of all documents relating to the appeal, the words "Tax Appeal" and the number of that appeal are included in the title of the appeal wherever the title occurs.

|

| (3) |

The Registrar shall establish and maintain a register for tax appeals.

|

|

| 7. |

Abatement of appeal

| (1) |

An appeal shall abate in any case where any filing fees due have not been paid in full within fourteen days from the date of notifying the appellant of the total amount of the fees payable by him.

|

| (2) |

Where an appellant is notified by post, the appellant shall be deemed, until the contrary is proved, to have received the notification at the time at which the letter would be delivered in the ordinary course of post.

|

|

| 8. |

Filing of statement of facts

The respondent shall file a statement of facts with the Registrar within thirty days of service upon him of the copy of memorandum of appeal by the appellant, during office hours.

|

| 9. |

Response and extension of time

| (1) |

The statement of facts filed under rule 8 shall—

| (a) |

be signed by the respondent;

|

| (b) |

giving an address for service of the respondent;

|

| (c) |

set out precisely the respondent's response to the memorandum of appeal and refer specifically to documentary evidence or other evidence which the respondent proposes to adduce at the hearing of the appeal.

|

|

| (2) |

The documentary evidence referred to in paragraph (1)(c) shall be annexed to the response.

|

| (3) |

The Court may extend the period specified in rule 8 if it is satisfied that, owing to any reasonable cause, the respondent was unable to file the statement of facts and documentary evidence within that period and there was unreasonable delay on the respondent's part.

|

|

| 10. |

Notice to parties to appear for hearing

| (1) |

Unless the parties otherwise agree, the Registrar shall give fifteen days' notice, in writing, to the parties of the date and place fixed for the hearing of the appeal.

|

| (2) |

The Court shall at the hearing of the appeal, hear the appellant and his witnesses first and the respondent shall be given an opportunity to cross examine the witness, if any.

|

| (3) |

At the close of the case of the appellant, the evidence of the respondent shall be heard, and the appellant shall be given the opportunity to cross examine each witnesses followed by reexamination by the respondent after which the parties may make oral or written submissions.

|

|

| 11. |

Reasons for dismissing appeal

| (1) |

Where on the day fixed, or on any other day to which the hearing may be adjourned, the appellant does not appear when the appeal is called out for hearing, the Court may dismiss the appeal.

|

| (2) |

Where it is proved to the satisfaction of the Court, that owing to absence of the appellant from Kenya, sickness, or other reasonable cause, the appellant was unable to attend the hearing of the appeal on the day and at the time fixed for that purpose, the Court may postpone the hearing for such reasonable time as it considers necessary.

|

| (3) |

Where the appellant appears and the respondent does not appear, the Court may proceed to hear the appeal ex parte.

|

|

| 12. |

Reinstatement of appeal

Where an appeal is dismissed under rule 11 (1), the appellant may apply to the Court for the reinstatement of the appeal, and the Court shall, where it is proved that the appellant was unable to appear for the hearing of the appeal due to any reasonable cause, readmit the appeal on such terms as it considers fit.

|

| 13. |

Rehearing of appeal

Where an appeal is heard ex parte, the respondent may apply to the Court for the rehearing of the appeal and the Court shall, where satisfied that the respondent was unable to appear for the hearing of the appeal due to any reasonable cause, rehear the appeal on such terms as it considers fit.

|

| 14. |

Limitations on grounds to rely on

The appellant shall not, except by leave of the Court and upon such terms as the Court may determine, rely on a ground other than a ground stated in the memorandum of appeal.

|

| 15. |

Admission of other evidence

The Court may, at the time of hearing of an appeal, admit other documentary or oral evidence not contained in the statement of facts of the appellant or respondent should it consider it necessary for determination of the appeal.

|

| 16. |

Admissibility of evidence

Save where the Court in a particular case otherwise directs copies of documents shall be admissible in evidence, but the Court may at any time direct that the original be produced notwithstanding that a copy has already been admitted in evidence.

|

| 17. |

Ancillary applications

| (1) |

Ancillary applications to the Court, if not made at the time of hearing, shall be made by notice of motion and titled in the matter of the tax appeal, supported by affidavit.

|

| (2) |

If no appeal has been filed, the motion shall be titled in the matter of the intended tax appeal.

|

|

| 18. |

Where a court decrees does not specify tax payable

Where a decree following the decision of the Court does not specify the amount of tax payable under the assessment as determined by the Court, the Commissioner shall for the purpose of the execution of that decree—

| (a) |

where the decision of the Court results in an amendment to the assessment filed with the Registrar, certify an amended assessment and serve it on the person assessed; or

|

| (b) |

where the decision does not result in an amendment to the assessment, file with the Registrar a statement signed by himself setting out the amount of tax payable under the notice of assessment served or the amended notice, as the case may be,

|

and the decree shall have effect as if it were a decree for the payment of the amount of tax set out in the notice or statement, as the case may be.

|

| 19. |

Fees

The scale of fees for the time being in force in civil matters in the Court shall apply in respect of filing fees and to all subsequent acts, applications or proceedings, in relation to the appeal.

|

| 20. |

Civil procedures to apply

The rules determining procedure in civil suits before the Court, to the extent to which those rules are not inconsistent with the Act or these Rules, shall apply to the tax appeal as if it were a civil suit.

|

| 21. |

Appeal to the Court of appeal

A person aggrieved by the decision of the Court may appeal to the Court of Appeal within fourteen days.

|

THE TAX APPEALS TRIBUNAL (APPEALS TO THE HIGH COURT) RULES

| 1. |

Citation

These Rules may be cited as the Tax Appeals Tribunal (Appeals to the High Court) Rules.

|

| 2. |

Interpretation

In these Rules, unless the context otherwise requires—

"address for service" means a place of residence or a place of business or last known address;

"appeal” means an appeal to the High Court under section 32 of the Act;

"Registrar" means the Registrar of the High Court.

|

| 3. |

Time for filing of memorandum of appeal

The appellant shall, within thirty days, after the date of service of a notice of appeal under section 32(1), file a memorandum of appeal with the Registrar and serve a copy on the respondent.

|

| 4. |

Extension of time for filing memorandum of appeal

The Court may extend the time specified in rule 3 if the Court is satisfied that, owing to absence from Kenya, sickness, or other reasonable cause, the appellant was unable to file the memorandum of appeal within that period and that there has been no unreasonable delay on the part of the appellant.

|

| 5. |

Memorandum of appeal

A memorandum of appeal shall—

| (a) |

be signed by the appellant;

|

| (b) |

contain an address of service of the appellant;

|

| (c) |

set out concisely under consecutively numbered distinct heads, the grounds of appeal without any arguments or narrative;

|

| (d) |

contain an index of all documents supporting the appeal with number of pages at which they appear; and

|

| (e) |

accompanied by a copy of the decision of the Tribunal and the notice of appeal.

|

|

| 6. |

Filing of memorandum of appeal and other documents

| (1) |

After the memorandum of appeal and the supporting documents have been filed, the Registrar shall stamp the memorandum of appeal and the documents filed, and number and enter the Appeal, as a Tax Appeal, in the register of tax appeals.

|

| (2) |

Upon entry of an appeal in the register of tax appeals, the Registrar shall ensure that, in respect of all documents relating to the appeal, the words "Tax Appeal" and the number of that appeal are included in the title of the appeal wherever the title occurs.

|

| (3) |

The Registrar shall establish and maintain a register for tax appeals.

|

|

| 7. |

Abatement of appeal

| (1) |

An appeal shall abate in any case where any filing fees due have not been paid in full within fourteen days from the date of notifying the appellant of the total amount of the fees payable by him.

|

| (2) |

Where an appellant is notified by post, the appellant shall be deemed, until the contrary is proved, to have received the notification at the time at which the letter would be delivered in the ordinary course of post.

|

|

| 8. |

Filing of statement of facts

The respondent shall file a statement of facts with the Registrar within thirty days of service upon him of the copy of memorandum of appeal by the appellant, during office hours.

|

| 9. |

Response and extension of time

| (1) |

The statement of facts filed under rule 8 shall—

| (a) |

be signed by the respondent;

|

| (b) |

giving an address for service of the respondent;

|

| (c) |

set out precisely the respondent's response to the memorandum of appeal and refer specifically to documentary evidence or other evidence which the respondent proposes to adduce at the hearing of the appeal.

|

|

| (2) |

The documentary evidence referred to in paragraph (1)(c) shall be annexed to the response.

|

| (3) |

The Court may extend the period specified in rule 8 if it is satisfied that, owing to any reasonable cause, the respondent was unable to file the statement of facts and documentary evidence within that period and there was unreasonable delay on the respondent's part.

|

|

| 10. |

Notice to parties to appear for hearing

| (1) |

Unless the parties otherwise agree, the Registrar shall give fifteen days' notice, in writing, to the parties of the date and place fixed for the hearing of the appeal.

|

| (2) |

The Court shall at the hearing of the appeal, hear the appellant and his witnesses first and the respondent shall be given an opportunity to cross examine the witness, if any.

|

| (3) |

At the close of the case of the appellant, the evidence of the respondent shall be heard, and the appellant shall be given the opportunity to cross examine each witnesses followed by reexamination by the respondent after which the parties may make oral or written submissions.

|

|

| 11. |

Reasons for dismissing appeal

| (1) |

Where on the day fixed, or on any other day to which the hearing may be adjourned, the appellant does not appear when the appeal is called out for hearing, the Court may dismiss the appeal.

|

| (2) |

Where it is proved to the satisfaction of the Court, that owing to absence of the appellant from Kenya, sickness, or other reasonable cause, the appellant was unable to attend the hearing of the appeal on the day and at the time fixed for that purpose, the Court may postpone the hearing for such reasonable time as it considers necessary.

|

| (3) |

Where the appellant appears and the respondent does not appear, the Court may proceed to hear the appeal ex parte.

|

|

| 12. |

Reinstatement of appeal

Where an appeal is dismissed under rule 11(1), the appellant may apply to the Court for the reinstatement of the appeal, and the Court shall, where it is proved that the appellant was unable to appear for the hearing of the appeal due to any reasonable cause, readmit the appeal on such terms as it considers fit.

|

| 13. |

Rehearing of appeal

Where an appeal is heard ex parte, the respondent may apply to the Court for the rehearing of the appeal and the Court shall, where satisfied that the respondent was unable to appear for the hearing of the appeal due to any reasonable cause, rehear the appeal on such terms as it considers fit.

|

| 14. |

Limitations on grounds to rely on

The appellant shall not, except by leave of the Court and upon such terms as the Court may determine, rely on a ground other than a ground stated in the memorandum of appeal.

|

| 15. |

Admission of other evidence

The Court may, at the time of hearing of an appeal, admit other documentary or oral evidence not contained in the statement of facts of the appellant or respondent should it consider it necessary for determination of the appeal.

|

| 16. |

Admissibility of evidence

Save where the Court in a particular case otherwise directs copies of documents shall be admissible in evidence, but the Court may at any time direct that the original be produced notwithstanding that a copy has already been admitted in evidence.

|

| 17. |

Ancillary applications

| (1) |

Ancillary applications to the Court, if not made at the time of hearing, shall be made by notice of motion and titled in the matter of the tax appeal, supported by affidavit.

|

| (2) |

If no appeal has been filed, the motion shall be titled in the matter of the intended tax appeal.

|

|

| 18. |

Where a court decrees does not specify tax payable

Where a decree following the decision of the Court does not specify the amount of tax payable under the assessment as determined by the Court, the Commissioner shall for the purpose of the execution of that decree—

| (a) |

where the decision of the Court results in an amendment to the assessment filed with the Registrar, certify an amended assessment and serve it on the person assessed; or

|

| (b) |

where the decision does not result in an amendment to the assessment, file with the Registrar a statement signed by himself setting out the amount of tax payable under the notice of assessment served or the amended notice, as the case may be,

|

and the decree shall have effect as if it were a decree for the payment of the amount of tax set out in the notice or statement, as the case may be.

|

| 19. |

Fees

The scale of fees for the time being in force in civil matters in the Court shall apply in respect of filing fees and to all subsequent acts, applications or proceedings, in relation to the appeal.

|

| 20. |

Civil procedures to apply

The rules determining procedure in civil suits before the Court, to the extent to which those rules are not inconsistent with the Act or these Rules, shall apply to the tax appeal as if it were a civil suit.

|

| 21. |

Appeal to the Court of appeal

A person aggrieved by the decision of the Court may appeal to the Court of Appeal within fourteen days.

|

THE TAX APPEALS TRIBUNAL (PROCEDURE) RULES

ARRANGEMENT OF RULES

| 3. |

Form and Filing of appeal

|

| 5. |

Statement of facts of appellant

|

| 10. |

Extension of time for submitting documents

|

| 11. |

Service on Commissioner

|

| 12. |

Lodging of material documents

|

| 13. |

Requirements as to binding of records and numbering of pages

|

| 14. |

Maintenance of register and files

|

| 15. |

Notice to parties to appear

|

| 16. |

Summons for witnesses

|

| 17. |

Mode of service of summons

|

| 18. |

Consequences of non-attendance

|

| 19. |

Setting aside, varying or reviewing of decisions or dismissal

|

| 21. |

Amendment of pleadings

|

| 22. |

Recording of evidence

|

| 23. |

Decision to be made in presence of parties

|

| 25. |

Evidence by affidavit and interrogatories

|

| 26. |

Publication of decisions

|

| 27. |

Tribunal to determine own procedure in certain matters

|

| 28. |

Revocation and saving

|

SCHEDULES

THE TAX APPEALS TRIBUNAL (PROCEDURE) RULES, 2015

| 1. |

Citation

These Rules may be cited as the Tax Appeals Tribunals (Procedure) Rules, 2015.

|

| 2. |

Interpretation

In these Rules, unless the context otherwise requires—

"appeal” has the meaning assigned to it under section 2 of the Act:

"appellant" means a person who has made an application to the Tribunal for review of a taxation decision under section 12, an extension of time under section 13 (3) or reinstatement of an application under section 27 (5):

"Chairperson" has the meaning assigned to it under section 2 of the Act;

“clerk" means a person designated as such under section 11 of the Act;

“commissioner's representative" means a person in charge of a Kenya Revenue Authority station where the tax dispute arose or the officer who communicated the tax decision;

"officer in charge of registry" means a person appointed by the Secretary to be in charge of tax appeals registry;

"respondent" means a party against whom an appeal or an application is filed;

"Secretary" has the meaning assigned to it under section 2 of the Act;

"tax decision” means—

| (b) |

a determination of the amount of tax payable or that will become payable by a taxpayer;

|

| (c) |

a determination of the amount that a tax representative, appointed person, director or controlling member is liable for;

|

| (d) |

a decision on an application by a self-assessment taxpayer;

|

| (f) |

a decision requiring repayment of a refund; or

|

| (g) |

a demand for a penalty.

|

|

| 3. |

Form and Filing of appeal

| (1) |

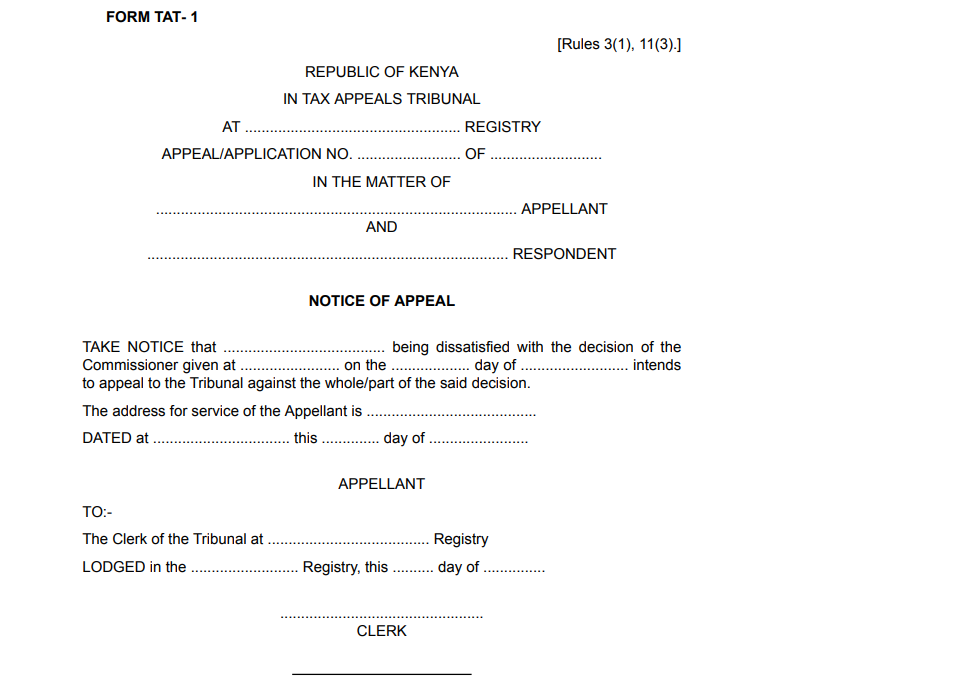

A notice of appeal to the Tribunal shall be—

| (a) |

in Form TAT-1 set out in the Schedule; and

|

| (b) |

submitted to the clerk of the Tribunal within thirty days upon receipt of the decision by the Commissioner.

|

|

| (2) |

The appellant shall, within fourteen days from the date of filing the notice of appeal, submit enough copies, as may be advised by the clerk, of—

|

|

| 4. |

Memorandum of appeal

| (1) |

A memorandum of appeal referred in rule 3(2) shall—

| (a) |

be signed by the appellant;

|

| (b) |

set out concisely under distinct heads, numbered consecutively, the grounds of appeal without argument or narrative;

|

| (c) |

contain an index of all documents in the appeal with number of pages at which they appear; and

|

| (d) |

be accompanied by a copy of the—

|

|

|

| 5. |

Statement of facts of appellant

| (1) |

Statement of fact signed by the appellant shall set out precisely all the facts on which the appeal is based and shall refer specifically to documentary evidence or other evidence which it is proposed to adduce at the hearing of the appeal.

|

| (2) |

The documentary evidence referred to in paragraph (1) shall be annexed to the statement of fact.

|

|

| 6. |

Principal registry

The principal registry of the Tribunal shall be at Nairobi, and the Chairperson may by notice in the Gazette designate other registries.

|

| 7. |

Titling of appeal

An appeal shall be titled as an "Appeal in the Tax Appeals Tribunal at the...................... Registry", stating the name of the registry in which it has been filed.

|

| 8. |

Status of appeal

The officer in charge of a registry shall within seven working days after receiving the appeal notify the Secretary of the particulars of that appeal.

|

| 9. |

Receipt of appeal

Upon receipt of an appeal, the clerk or officer in charge of a registry shall—

| (a) |

stamp, date and sign all the copies of the appeal;

|

| (b) |

retain sufficient copies for the Tribunal; and

|

| (c) |

return one copy to be served on the Commissioner in accordance with rule 12 of these Rules.

|

|

| 10. |

Extension of time for submitting documents

| (1) |

Where the documents referred to in rule 3(2) are not filed within the time specified therein, the Tribunal may, upon application in writing, extend the time for submitting the documents.

|

| (2) |

An application for extension of time referred to in rule 10(1) shall be—

| (a) |

supported by an affidavit stating reasons why the applicant was unable to submit the documents in time;

|

| (b) |

served on the respondent by the applicant within two days of filing with the clerk.

|

|

| (3) |

The Tribunal may grant the extension of time if it is satisfied that the applicant was unable to submit the documents in time for the following reasons—

| (c) |

any other reasonable cause.

|

|

| (4) |

The respondent may respond to the application by filing an affidavit within fourteen days from the date of service of the application.

|

| (5) |

The Tribunal shall set down the hearing date for the application.

|

|

| 11. |

Service on Commissioner

| (1) |

An appellant shall within two days of filing an appeal with the Tribunal serve a copy on the Commissioner or the Commissioner' s representative.

|

| (2) |

Service on the Commissioner under paragraph (1) shall be by delivering or tendering to him or his representative a copy of the appeal.

|

| (3) |

An acknowledgement of service on the appeal shall be signed by the Commissioner or his representative, which shall be returned to the clerk as proof of service.

|

|

| 12. |

Lodging of material documents

Commissioner shall, within thirty days after being served with an appeal under rule 11 file enough copies as may be advised by the clerk, of—

| (b) |

a statement giving reasons for the tax decision; and

|

| (c) |

all documents which are necessary to enable the Tribunal to review the decision.

|

|

| 13. |

Requirements as to binding of records and numbering of pages

The appeal may be bound with a cover and pages numbered consecutively.

|

| 14. |

Maintenance of register and files

| (1) |

The officer in charge of a registry shall maintain—

| (a) |

a register of all applications and appeals in every year, according to the order in which they are filed and shall contain—

| (iii) |

the name and address of the appellant or applicant; |

| (iv) |

nature of the tax dispute or application; |

| (v) |

the date of the hearing; |

| (vi) |

the decision or order of the Tribunal and the date on which it was made; and |

|

| (b) |

a file for each appeal containing—

| (i) |

a copy of the memorandum of the appeal and statements of facts of the appellant and the respondent; |

| (ii) |

a list of all material documents including those requested for by the Tribunal; |

| (iii) |

the record of the proceedings and the evidence given by the parties and their witnesses; |

| (iv) |

summons and notices issued by the Tribunal; |

| (v) |

the submissions of the parties; |

| (vi) |

notices of the decision; and |

| (vii) |

the decision of the Tribunal. |

|

|

|

| 15. |

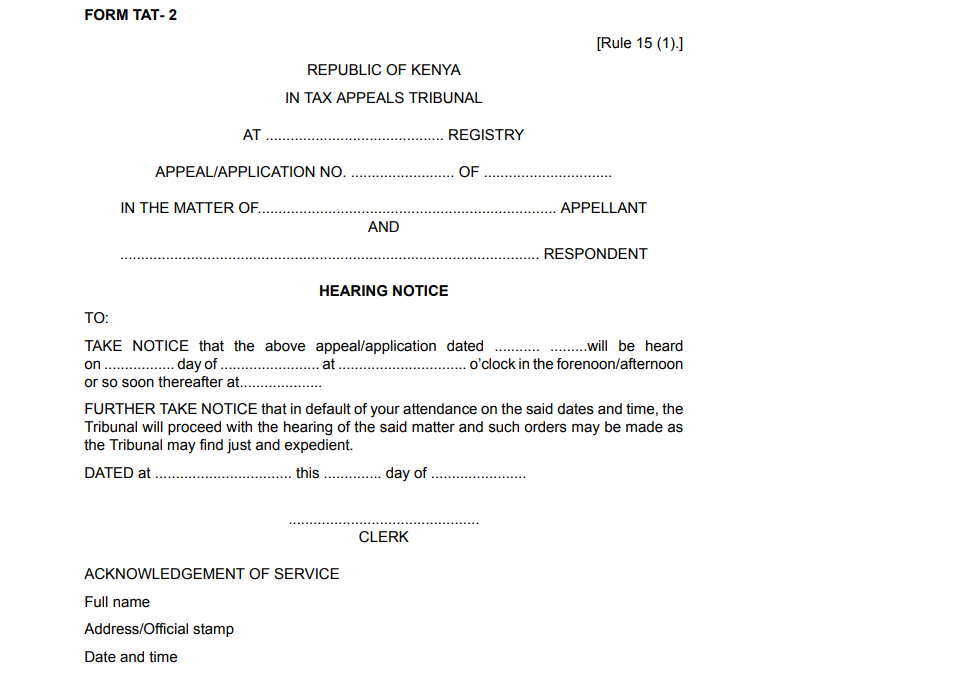

Notice to parties to appear

| (1) |

The Clerk shall upon consultation with the Chairperson give all parties to an appeal not less than fourteen days' notice of the date fixed for the first hearing of the appeal in Form TAT-2 in the Schedule to these Rules.

|

| (2) |

Dates for subsequent hearings may be fixed by the Tribunal.

|

|

| 16. |

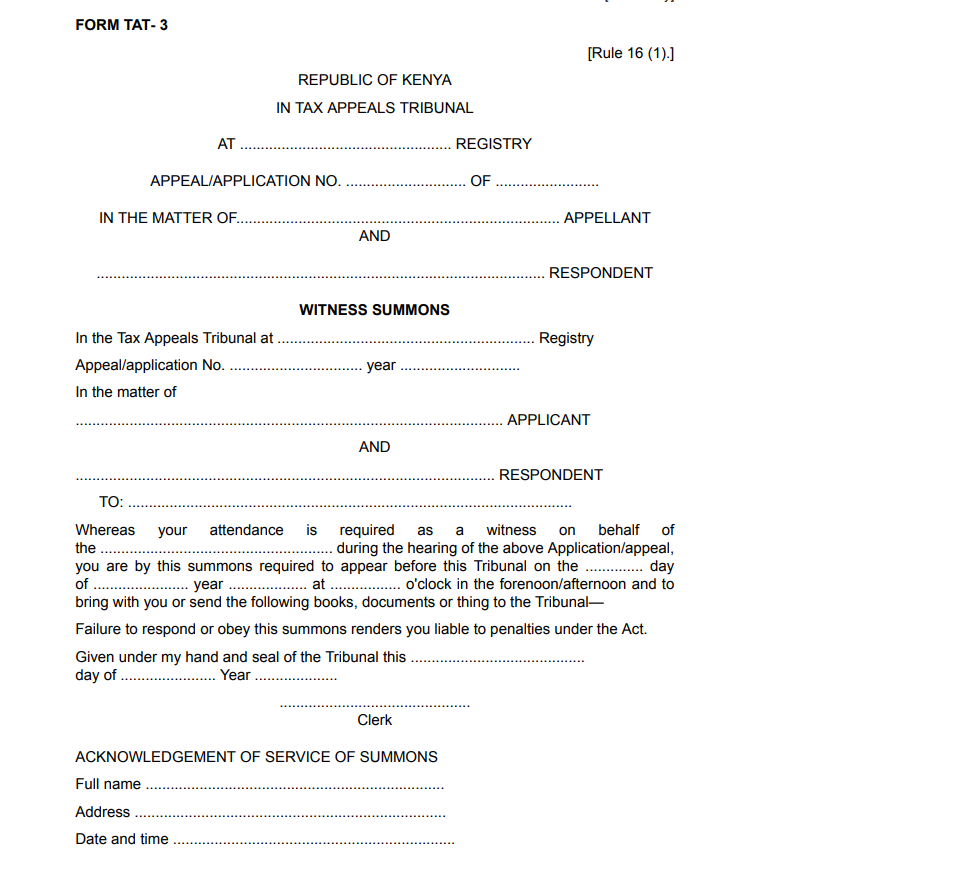

Summons for witnesses

| (1) |

The Clerk shall, before the date of the hearing of an appeal, serve summons in Form TAT-3 in the Schedule to a witness, requiring him to attend the hearing of an appeal at a date, time and place specified in the summons.

|

| (2) |

A person summoned as a witness before the Tribunal, excluding the Kenya Revenue Authority officers, is entitled to be paid allowances paid to the witnesses in High Court.

|

|

| 17. |

Mode of service of summons

| (1) |

Summons shall be served personally on the person named in the summons by delivering or tendering to him the original summons.

|

| (2) |

A person upon whom a summon or notice is served shall sign or mark in acknowledgement of receipt of the summons or notice at the back of the duplicate of the summons or notice, which shall then be returned to the Tribunal.

|

| (3) |

Where a person refuses to acknowledge receipt of summons or notice under paragraph (2), the person who is serving the summons or notice shall record in writing the refusal on the back of the notice or summons.

|

| (4) |

Where it is not possible to effect personal service of a summon or notice in the manner provided in this rule, service of the summon or notice may be made by—

| (a) |

leaving the duplicate of the summons or notice with any adult person residing with him, an adult member of the family, his employer or employee; or

|

| (b) |

affixing the duplicate to a conspicuous place in the house or homestead in which the person named in the summons or notice ordinarily resides or by affixing the duplicate in a conspicuous place in his office or place of work or posted to the last known address and also to a conspicuous place in the Tribunal offices; or

|

| (c) |

publishing the particulars of the summons or notice in a newspaper circulating it in the area or any other media.

|

|

| (5) |

Every summons or notice issued under these Rules and requiring service shall be served by an officer of the Tribunal, a court process server, or any other person authorized to do so by the Tribunal including a police officer.

|

| (6) |

Any notice or summons served on an advocate, representative, or tax agent, of a party, by registered post or by leaving it at the chambers or office and whether it is for the personal appearance of the party or not, shall be presumed to be duly communicated and, unless the Tribunal otherwise directs, shall be effectual for all purposes as if it had been served on the party in person.

|

| (7) |

A summon, warrant, order, notice or other formal document issued by the Tribunal shall be signed by the Clerk, and shall be stamped with the stamp of the Tribunal.

|

|

| 18. |

Consequences of non-attendance

| (1) |

When neither party attends on the day fixed for hearing, if satisfied that the notice of hearing was duly served to the parties, the Tribunal may dismiss the appeal or give such orders that it may deem appropriate.

|

| (2) |

Where only the appellant attends and if the Tribunal is satisfied that the notice of hearing was—

| (a) |

duly served, it may proceed ex parte;

|

| (b) |

not duly served, it shall direct a second notice to be served; or

|

| (c) |

not served in sufficient time or for other reasonable cause, the respondent was unable to attend, it shall postpone the hearing.

|

|

| (3) |

Where only the respondent attends and if the Tribunal is satisfied that notice of hearing was—

| (a) |

duly served, it may dismiss the appeal;

|

| (b) |

not duly served, it shall direct a second notice to be served; or

|

| (c) |

not served in sufficient time or for other reasonable cause, the appellant was unable to attend, it shall postpone the hearing.

|

|

|

| 19. |

Setting aside, varying or reviewing of decisions or dismissal

Upon an application by the applicant, the Tribunal, stating the reasons, may set aside, vary or review a decision made under these Rules.

|

| 20. |

Order of addresses

| (1) |

The Tribunal shall at the hearing of an appeal, hear the appellant and his witnesses first and the respondent shall be given an opportunity to cross examine the witness, if any.

|

| (2) |

Before the case is concluded, the evidence of the respondent shall be heard, and the appellant shall be given the opportunity to cross examine each witness followed by re-examination by the respondent after which the parties may make oral or written submissions.

|

| (3) |

The Tribunal may, at any time, put questions to either party or to any witness, and may, at its discretion, call additional evidence as it may be necessary for further clarification of the issues raised at the hearing of the appeal.

|

| (4) |

The Tribunal may, for sufficient reason, at any time after beginning the hearing of the appeal, adjourn the hearing; and in every such situation, the Tribunal shall fix another convenient day for further hearing.

|

|

| 21. |

Amendment of pleadings

A party may at any time before the closure of the case, orally apply to amend its pleadings and the Tribunal may, at its discretion, allow such application on such terms and conditions including granting leave to the other party to amend its pleadings provided the amendments do not raise new issues.

|

| 22. |

Recording of evidence

| (1) |

The evidence of the parties and that of a witness shall be recorded by the members of the Tribunal, or by a person authorized to do so, in a form to be decided upon by the members and when completed shall be signed by the members of the Tribunal at that proceeding.

|

| (2) |

Notwithstanding paragraph (1), the evidence given at the hearing of an appeal may be recorded in short hand or by mechanical means, and the transcript of anything recorded shall, if certified by members of the Tribunal at that proceeding to be correct, be deemed to be a true record of the evidence for the purposes of the proceeding.

|

|

| 23. |

Decision to be made in presence of parties

| (1) |

After concluding the hearing of the evidence and submissions of the parties, the Tribunal shall, as soon as practicable, make a written decision which shall, on notice to both parties, be read in their presence or of their advocates or representatives and shall cause a copy, duly signed by the members of the Tribunal which heard the appeal, to be served to each party to the proceeding.

|

| (2) |

The decision of the Tribunal shall be determined by a majority of the members present and voting at the meeting, and in the case of an equality of votes the chairperson shall have a casting vote in addition to his deliberative vote.

|

|

| 24. |

Contents of decision

The written decision of the Tribunal shall contain—

| (a) |

the nature of the appeal;

|

| (b) |

summary of the facts of the case;

|

| (c) |

the issues for determination citing the relevant tax law;

|

| (d) |

the arguments by the appellant and the respondent on the issues;

|

| (e) |

a summary of the relevant evidence produced before the Tribunal and the findings on each issue;

|

| (f) |

the relief or remedy, if any, to which the appellant or respondent is entitled; and

|

| (g) |

an order for costs or other relief.

|

|

| 25. |

Evidence by affidavit and interrogatories

| (1) |

Where the Tribunal requires evidence to be received by means of affidavits or interrogatories, the affidavits or interrogatories and the answers shall be by such means and in such form as the Tribunal may direct.

|

| (2) |

In any proceeding where the evidence of a witness who resides outside Kenya is necessary, the Tribunal may issue a commission or letter of request to examine that witness abroad.

|

| (3) |

A party may present its evidence to the Tribunal either orally, by affidavit, statement on oath or by combination of any of these methods.

|

|

| 26. |

Publication of decisions

The Secretary of the Tribunal shall within seven days from the date of making the decision, submit a copy of that decision to the Kenya Law Reports for publication.

|

| 27. |

Tribunal to determine own procedure in certain matters

The Tribunal may determine an appropriate procedure where there are no applicable procedures under these Rules or the Act.

|

| 28. |

Revocation and saving

| (1) |

The following Rules are revoked—

| (a) |

the Income Tax (Local Committee) Rules, 1974 (L.N. No. 7/1974);

|

| (b) |

the Income Tax (Tribunal Rules) Rules, 1974 (L.N. No. 5/1974);

|

| (c) |

the Customs and Excise (Appeals) Rules, 2000 (L.N. No. 67/2000); and

|

| (d) |

the Value Added Tax (Appeals) Rules, 1990 (L.N. No. 229/1990).

|

|

| (2) |

Notwithstanding the provisions of paragraph (1)—

| (a) |

all things lawfully done under the repealed rules which are in force and effect immediately before the commencement of these rules including decisions or directions given under the repealed rules shall so far as consistent with these Rules and anything done under them continue to be in force and effect after the commencement; and

|

| (b) |

where any proceedings in respect of an appeal have been commenced before the date of commencement of these Rules, any step in the proceedings taken in accordance with the repealed Rules shall be deemed to have been validly taken for purposes of these Rules.

|

|

|

THE TAX APPEALS TRIBUNAL (PROCEDURE) RULES, 2015

| 1. |

Citation

These Rules may be cited as the Tax Appeals Tribunals (Procedure) Rules, 2015.

|

| 2. |

Interpretation

In these Rules, unless the context otherwise requires—

"appeal” has the meaning assigned to it under section 2 of the Act:

"appellant" means a person who has made an application to the Tribunal for review of a taxation decision under section 12, an extension of time under section 13 (3) or reinstatement of an application under section 27(5);

"Chairperson" has the meaning assigned to it under section 2 of the Act;

“clerk" means a person appointed as such under section 11 of the Act;

“Commissioner's representative" means a person authorized to appear on behalf of the Commissioner before the Tribunal;

"officer in charge of registry" means a person appointed by the Secretary to be in charge of tax appeals registry;

"respondent" means a party against whom an appeal or an application is filed;

"Secretary" has the meaning assigned to it under section 2 of the Act;

"tax decision” means—

| (b) |

a determination of the amount of tax payable or that will become payable by a taxpayer;

|

| (c) |

a determination of the amount that a tax representative, appointed person, director or controlling member is liable for;

|

| (d) |

a decision on an application by a self-assessment taxpayer;

|

| (f) |

a decision requiring repayment of a refund; or

|

| (g) |

a demand for a penalty.

|

[L.N. 105/2016, r. 2.]

|

| 3. |

Form and Filing of appeal

| (1) |

A notice of appeal to the Tribunal shall be—

| (a) |

in Form TAT-1 set out in the Schedule; and

|

| (b) |

submitted to the clerk of the Tribunal within thirty days upon receipt of the decision by the Commissioner.

|

|

| (2) |

The appellant shall, within fourteen days from the date of filing the notice of appeal, submit enough copies, as may be advised by the clerk, of—

|

|

| 4. |

Memorandum of appeal

| (1) |

A memorandum of appeal referred in rule 3(2) shall—

| (a) |

be signed by the appellant;

|

| (b) |

set out concisely under distinct heads, numbered consecutively, the grounds of appeal without argument or narrative:

|

| (c) |

contain an index of all documents in the appeal with number of pages at which they appear; and

|

| (d) |

be accompanied by a copy of the—

|

|

|

| 5. |

Statement of facts of appellant

| (1) |

Statement of fact signed by the appellant shall set out precisely all the facts on which the appeal is based and shall refer specifically to documentary evidence or other evidence which it is proposed to adduce at the hearing of the appeal.

|

| (2) |

The documentary evidence referred to in paragraph (1) shall be annexed to the statement of fact.

|

|

| 6. |

Principal registry

The principal registry of the Tribunal shall be at Nairobi, and the Chairperson may by notice in the Gazette designate other registries.

|

| 7. |

Titling of appeal

An appeal shall be titled as an "Appeal in the Tax Appeals Tribunal at the...................... Registry", stating the name of the registry in which it has been filed.

|

| 8. |

Status of appeal

The officer in charge of a registry shall within seven working days after receiving the appeal notify the Secretary of the particulars of that appeal.

|

| 9. |

Receipt of appeal

Upon receipt of an appeal, the clerk or officer in charge of a registry shall—

| (a) |

stamp, date and sign all the copies of the appeal;

|

| (b) |

retain sufficient copies for the Tribunal; and

|

| (c) |

return one copy to be served on the Commissioner in accordance with rule 12 of these Rules.

|

|

| 10. |

Extension of time for submitting documents

| (1) |

Where the documents referred to in rule 3(2) are not filed within the time specified therein, the Tribunal may, upon application in writing, extend the time for submitting the documents.

|

| (2) |

An application for extension of time referred to in rule 10(1) shall be—

| (a) |

supported by an affidavit stating reasons why the applicant was unable to submit the documents in time;

|

| (b) |

served on the respondent by the applicant within two days of filing with the clerk.

|

|

| (3) |

The Tribunal may grant the extension of time if it is satisfied that the applicant was unable to submit the documents in time for the following reasons—

| (c) |

any other reasonable cause.

|

|

| (4) |

The respondent may respond to the application by filing an affidavit within fourteen days from the date of service of the application.

|

| (5) |

The Tribunal shall set down the hearing date for the application.

|

|

| 11. |

Service on Commissioner

| (1) |

An appellant shall within two days of filing an appeal with the Tribunal serve a copy on the Commissioner or the Commissioner' s representative.

|

| (2) |

Service on the Commissioner under paragraph (1) shall be by delivering or tendering to him or his representative a copy of the appeal.

|

| (3) |

An acknowledgement of service on the appeal shall be signed by the Commissioner or his representative, which shall be returned to the clerk as proof of service.

|

|

| 12. |

Lodging of material documents

The Commissioner shall, within thirty days of being served with an appeal under rule 11, file nine copies or such number of copies as, the Tribunal, may advise, of—

| (b) |

a statement giving reasons for the tax decision; and

|

| (c) |

all documents which are necessary to enable the Tribunal to review the decision. [L.N. 105/2016, r. 3.]

|

|

| 13. |

Requirements as to binding of records and numbering of pages

The appeal may be bound with a cover and pages numbered consecutively.

|

| 14. |

Maintenance of register and files

| (1) |

The officer in charge of a registry shall maintain—

| (a) |

a register of all applications and appeals in every year, according to the order in which they are filed and shall contain—

| (iii) |

the name and address of the appellant or applicant; |

| (iv) |

nature of the tax dispute or application; |

| (v) |

the date of the hearing; |

| (vi) |

the decision or order of the Tribunal and the date on which it was made; and |

|

| (b) |

a file for each appeal containing—

| (i) |

a copy of the memorandum of the appeal and statements of facts of the appellant and the respondent; |

| (ii) |

a list of all material documents including those requested for by the Tribunal; |

| (iii) |

the record of the proceedings and the evidence given by the parties and their witnesses; |

| (iv) |

summons and notices issued by the Tribunal; |

| (v) |

the submissions of the parties; |

| (vi) |

notices of the decision; and |

| (vii) |

the decision of the Tribunal. |

|

|

|

| 15. |

Notice to parties to appear

| (1) |

The Clerk shall upon consultation with the Chairperson give all parties to an appeal not less than fourteen days' notice of the date fixed for the first hearing of the appeal in Form TAT-2 in the Schedule to these Rules.

|

| (2) |

Dates for subsequent hearings may be fixed by the Tribunal.

|

|

| 16. |

Summons for witnesses

| (1) |

The Clerk shall, before the date of the hearing of an appeal, serve summons in Form TAT-3 in the Schedule to a witness, requiring him to attend the hearing of an appeal at a date, time and place specified in the summons.

|

| (2) |

A person summoned as a witness before the Tribunal, excluding the Kenya Revenue Authority officers, is entitled to be paid allowances paid to the witnesses in High Court.

|

|

| 17. |

Mode of service of summons

| (1) |

Summons shall be served personally on the person named in the summons by delivering or tendering to him the original summons.

|

| (2) |

A person upon whom a summon or notice is served shall sign or mark in acknowledgement of receipt of the summons or notice at the back of the duplicate of the summons or notice, which shall then be returned to the Tribunal.

|

| (3) |

Where a person refuses to acknowledge receipt of summons or notice under paragraph (2), the person who is serving the summons or notice shall record in writing the refusal on the back of the notice or summons.

|

| (4) |

Where it is not possible to effect personal service of a summon or notice in the manner provided in this rule, service of the summon or notice may be made by—

| (a) |

leaving the duplicate of the summons or notice with any adult person residing with him, an adult member of the family, his employer or employee; or

|

| (b) |

affixing the duplicate to a conspicuous place in the house or homestead in which the person named in the summons or notice ordinarily resides or by affixing the duplicate in a conspicuous place in his office or place of work or posted to the last known address and also to a conspicuous place in the Tribunal offices; or

|

| (c) |

publishing the particulars of the summons or notice in a newspaper circulating it in the area or any other media.

|

|

| (5) |

Every summons or notice issued under these Rules and requiring service shall be served by an officer of the Tribunal, a court process server, or any other person authorized to do so by the Tribunal including a police officer.

|

| (6) |

Any notice or summons served on an advocate, representative, or tax agent, of a party, by registered post or by leaving it at the chambers or office and whether it is for the personal appearance of the party or not, shall be presumed to be duly communicated and, unless the Tribunal otherwise directs, shall be effectual for all purposes as if it had been served on the party in person.

|

| (7) |

A summon, warrant, order, notice or other formal document issued by the Tribunal shall be signed by the Clerk, and shall be stamped with the stamp of the Tribunal.

|

|

| 17A. |

Warrant of arrest

Where, without sufficient cause, a witness fails to appear before the Tribunal when summoned, the Tribunal may on the proof that the witness was properly served with the summons, issue a warrant of arrest for the witness to be brought before the Tribunal on the date, time and place specified in the warrant. [L.N. 105/2016, r. 4.]

|

| 18. |

Consequences of non-attendance

| (1) |

When neither party attends on the day fixed for hearing, if satisfied that the notice of hearing was duly served to the parties, the Tribunal may dismiss the appeal or give such orders that it may deem appropriate.

|

| (2) |

Where only the appellant attends and if the Tribunal is satisfied that the notice of hearing was—

| (a) |

duly served, it may proceed ex parte;

|

| (b) |

not duly served, it shall direct a second notice to be served; or

|

| (c) |

not served in sufficient time or for other reasonable cause, the respondent was unable to attend, it shall postpone the hearing.

|

|

| (3) |

Where only the respondent attends and if the Tribunal is satisfied that notice of hearing was—

| (a) |

duly served, it may dismiss the appeal;

|

| (b) |

not duly served, it shall direct a second notice to be served; or

|

| (c) |

not served in sufficient time or for other reasonable cause, the appellant was unable to attend, it shall postpone the hearing.

|

|

|

| 19. |

Setting aside, varying or reviewing of decisions or dismissal

Upon an application by the applicant, the Tribunal, stating the reasons, may set aside, vary or review a decision made under these Rules.

|

| 20. |

Order of addresses

| (1) |

The Tribunal shall at the hearing of an appeal, hear the appellant and his witnesses first and the respondent shall be given an opportunity to cross examine the witness, if any.

|

| (2) |

Before the case is concluded, the evidence of the respondent shall be heard, and the appellant shall be given the opportunity to cross examine each witness followed by re-examination by the respondent after which the parties may make oral or written submissions.

|

| (3) |

The Tribunal may, at any time, put questions to either party or to any witness, and may, at its discretion, call additional evidence as it may be necessary for further clarification of the issues raised at the hearing of the appeal.

|

| (4) |

The Tribunal may, for sufficient reason, at any time after beginning the hearing of the appeal, adjourn the hearing; and in every such situation, the Tribunal shall fix another convenient day for further hearing.

|

|

| 21. |

Amendment of pleadings

A party may at any time before the closure of the case, orally apply to amend its pleadings and the Tribunal may, at its discretion, allow such application on such terms and conditions including granting leave to the other party to amend its pleadings provided the amendments do not raise new issues.

|

| 22. |

Recording of evidence

| (1) |

The evidence of the parties and that of a witness shall be recorded by the members of the Tribunal, or by a person authorized to do so, in a form to be decided upon by the members and when completed shall be signed by the members of the Tribunal at that proceeding.

|

| (2) |

Notwithstanding paragraph (1), the evidence given at the hearing of an appeal may be recorded in short hand or by mechanical means, and the transcript of anything recorded shall, if certified by members of the Tribunal at that proceeding to be correct, be deemed to be a true record of the evidence for the purposes of the proceeding.

|

|

| 23. |

Decision to be made in presence of parties

| (1) |

After concluding the hearing of the evidence and submissions of the parties, the Tribunal shall, as soon as practicable, make a written decision which shall, on notice to both parties, be read in their presence or of their advocates or representatives and shall cause a copy, duly signed by the members of the Tribunal which heard the appeal, to be served to each party to the proceeding.

|

| (2) |

The decision of the Tribunal shall be determined by a majority of the members present and voting at the meeting, and in the case of an equality of votes the chairperson shall have a casting vote in addition to his deliberative vote.

|

|

| 24. |

Contents of decision

The written decision of the Tribunal shall contain—

| (a) |

the nature of the appeal;

|

| (b) |

summary of the facts of the case;

|

| (c) |

the issues for determination citing the relevant tax law;

|

| (d) |

the arguments by the appellant and the respondent on the issues;

|

| (e) |

a summary of the relevant evidence produced before the Tribunal and the findings on each issue;

|

| (f) |

the relief or remedy, if any, to which the appellant or respondent is entitled; and

|

| (g) |

an order for costs or other relief.

|

|

| 25. |

Evidence by affidavit and interrogatories

| (1) |

Where the Tribunal requires evidence to be received by means of affidavits or interrogatories, the affidavits or interrogatories and the answers shall be by such means and in such form as the Tribunal may direct.

|

| (2) |

In any proceeding where the evidence of a witness who resides outside Kenya is necessary, the Tribunal may issue a commission or letter of request to examine that witness abroad.

|

| (3) |

A party may present its evidence to the Tribunal either orally, by affidavit, statement on oath or by combination of any of these methods.

|

|

| 26. |

Publication of decisions

The Secretary of the Tribunal shall within fourteen days from the date of making the decision, submit a copy of that decision to the Kenya Law Reports for publication. [L.N. 105/2016, r. 5.]

|

| 27. |

Tribunal to determine own procedure in certain matters

The Tribunal may determine an appropriate procedure where there are no applicable procedures under these Rules or the Act.

|

| 28. |

Revocation and saving

| (1) |

The following Rules are revoked—

| (a) |

the Income Tax (Local Committee) Rules, 1974 (L.N. No. 7/1974);

|

| (b) |

the Income Tax (Tribunal Rules) Rules, 1974 (L.N. No. 5/1974);

|

| (c) |

the Customs and Excise (Appeals) Rules, 2000 (L.N. No. 67/2000); and

|

| (d) |

the Value Added Tax (Appeals) Rules, 1990 (L.N. No. 229/1990).

|

|

| (2) |

Notwithstanding the provisions of paragraph (1)—

| (a) |

all things lawfully done under the repealed rules which are in force and effect immediately before the commencement of these rules including decisions or directions given under the repealed rules shall so far as consistent with these Rules and anything done under them continue to be in force and effect after the commencement; and

|

| (b) |

where any proceedings in respect of an appeal have been commenced before the date of commencement of these Rules, any step in the proceedings taken in accordance with the repealed Rules shall be deemed to have been validly taken for purposes of these Rules.

|

|

|

THE TAX APPEALS TRIBUNAL (PROCEDURE) RULES, 2015

| 1. |

Citation

These Rules may be cited as the Tax Appeals Tribunals (Procedure) Rules, 2015.

|

| 2. |

Interpretation

In these Rules, unless the context otherwise requires—

"appeal” has the meaning assigned to it under section 2 of the Act:

"appellant" means a person who has made an application to the Tribunal for review of a taxation decision under section 12, an extension of time under section 13 (3) or reinstatement of an application under section 27(5);

"Chairperson" has the meaning assigned to it under section 2 of the Act;

“clerk" means a person appointed as such under section 11 of the Act;

“Commissioner's representative" means a person authorized to appear on behalf of the Commissioner before the Tribunal;

"officer in charge of registry" means a person appointed by the Secretary to be in charge of tax appeals registry;

"respondent" means a party against whom an appeal or an application is filed;

"Secretary" has the meaning assigned to it under section 2 of the Act;

"tax decision” means—

| (b) |

a determination of the amount of tax payable or that will become payable by a taxpayer;

|

| (c) |

a determination of the amount that a tax representative, appointed person, director or controlling member is liable for;

|

| (d) |

a decision on an application by a self-assessment taxpayer;

|

| (f) |

a decision requiring repayment of a refund; or

|

| (g) |

a demand for a penalty.

|

[L.N. 105/2016, r. 2.]

|

| 3. |

Form and Filing of appeal

| (1) |

A notice of appeal to the Tribunal shall be—

| (a) |

in Form TAT-1 set out in the Schedule; and

|

| (b) |

submitted electronically or physically to the clerk of the Tribunal within thirty days upon receipt of the decision by the Commissioner.

|

|

| (2) |

The appellant shall, within fourteen days from the date of filing the notice of appeal, submit enough copies, as may be advised by the clerk, of—

|

|

| 4. |

Memorandum of appeal

| (1) |

A memorandum of appeal referred in rule 3(2) shall—

| (a) |

be signed by the appellant;

|

| (b) |

set out concisely under distinct heads, numbered consecutively, the grounds of appeal without argument or narrative:

|

| (c) |

contain an index of all documents in the appeal with number of pages at which they appear; and

|

| (d) |

be accompanied by a copy of the—

|

|

|

| 5. |

Statement of facts of appellant

| (1) |

Statement of fact signed by the appellant shall set out precisely all the facts on which the appeal is based and shall refer specifically to documentary evidence or other evidence which it is proposed to adduce at the hearing of the appeal.

|

| (2) |

The documentary evidence referred to in paragraph (1) shall be annexed to the statement of fact.

|

|

| 6. |

Principal registry

The principal registry of the Tribunal shall be at Nairobi, and the Chairperson may by notice in the Gazette designate other registries.

|

| 7. |

Titling of appeal

An appeal shall be titled as an "Appeal in the Tax Appeals Tribunal at the...................... Registry", stating the name of the registry in which it has been filed.

|

| 8. |

Status of appeal

The officer in charge of a registry shall within seven working days after receiving the appeal notify the Secretary of the particulars of that appeal.

|

| 9. |

Receipt of appeal

Upon receipt of an appeal, the clerk or officer in charge of a registry shall—

| (a) |

stamp, date and sign all the copies of the appeal;

|

| (b) |

retain sufficient copies for the Tribunal; and

|

| (c) |

return one copy to be served on the Commissioner in accordance with rule 12 of these Rules.

|

|

| 10. |

Extension of time for submitting documents

| (1) |

Where the documents referred to in rule 3(2) are not filed within the time specified therein, the Tribunal may, upon application in writing, extend the time for submitting the documents.

|

| (2) |

An application for extension of time referred to in rule 10(1) shall be—

| (a) |

supported by an affidavit stating reasons why the applicant was unable to submit the documents in time;

|

| (b) |

served on the respondent by the applicant within two days of filing with the clerk.

|

|

| (3) |

The Tribunal may grant the extension of time if it is satisfied that the applicant was unable to submit the documents in time for the following reasons—

| (c) |

any other reasonable cause.

|

|

| (4) |

The respondent may respond to the application by filing an affidavit within fourteen days from the date of service of the application.

|

| (5) |

The Tribunal shall set down the hearing date for the application.

|

|

| 11. |

Service on Commissioner

| (1) |

An appellant shall within two days of filing an appeal with the Tribunal serve a copy on the Commissioner or the Commissioner' s representative.

|

| (2) |

Service on the Commissioner under paragraph (1) shall be by delivering or tendering to him or his representative a copy of the appeal.

|

| (3) |

An acknowledgement of service on the appeal shall be signed by the Commissioner or his representative, which shall be returned to the clerk as proof of service.

|

|

| 12. |

Lodging of material documents

The Commissioner shall, within thirty days of being served with an appeal under rule 11, file nine copies or such number of copies as, the Tribunal, may advise, of—

| (b) |

a statement giving reasons for the tax decision; and

|

| (c) |

all documents which are necessary to enable the Tribunal to review the decision. [L.N. 105/2016, r. 3.]

|

|

| 13. |

Requirements as to binding of records and numbering of pages

The appeal may be bound with a cover and pages numbered consecutively.

|

| 14. |

Maintenance of register and files

| (1) |

The officer in charge of a registry shall maintain—

| (a) |

a register of all applications and appeals in every year, according to the order in which they are filed and shall contain—

| (iii) |

the name and address of the appellant or applicant; |

| (iv) |

nature of the tax dispute or application; |

| (v) |

the date of the hearing; |

| (vi) |

the decision or order of the Tribunal and the date on which it was made; and |

|

| (b) |

a file for each appeal containing—

| (i) |

a copy of the memorandum of the appeal and statements of facts of the appellant and the respondent; |

| (ii) |

a list of all material documents including those requested for by the Tribunal; |

| (iii) |

the record of the proceedings and the evidence given by the parties and their witnesses; |

| (iv) |

summons and notices issued by the Tribunal; |

| (v) |

the submissions of the parties; |

| (vi) |

notices of the decision; and |

| (vii) |

the decision of the Tribunal. |

|

|

|

| 15. |

Notice to parties to appear

| (1) |

The Clerk shall upon consultation with the Chairperson give all parties to an appeal not less than fourteen days' notice of the date fixed for the first hearing of the appeal in Form TAT-2 in the Schedule to these Rules.

|

| (2) |

Dates for subsequent hearings may be fixed by the Tribunal.

|

|

| 16. |

Summons for witnesses

| (1) |

The Clerk shall, before the date of the hearing of an appeal, serve summons in Form TAT-3 in the Schedule to a witness, requiring him to attend the hearing of an appeal at a date, time and place specified in the summons.

|

| (2) |

A person summoned as a witness before the Tribunal, excluding the Kenya Revenue Authority officers, is entitled to be paid allowances paid to the witnesses in High Court.

|

|

| 17. |

Mode of service of summons

| (1) |

Summons shall be served personally on the person named in the summons by delivering or tendering to him the original summons or through electronic mail service to the last known and used email address or mobile number.

|

| (2) |

A person upon whom a summon or notice is served shall sign or mark in acknowledgement of receipt of the summons or notice at the back of the duplicate of the summons or notice, which shall then be returned to the Tribunal.

|

| (3) |

Where a person refuses to acknowledge receipt of summons or notice under paragraph (2), the person who is serving the summons or notice shall record in writing the refusal on the back of the notice or summons.

|

| (4) |

Where it is not possible to effect personal service of a summon or notice in the manner provided in this rule, service of the summon or notice may be made by—

| (a) |

leaving the duplicate of the summons or notice with any adult person residing with him, an adult member of the family, his employer or employee; or

|

| (b) |

affixing the duplicate to a conspicuous place in the house or homestead in which the person named in the summons or notice ordinarily resides or by affixing the duplicate in a conspicuous place in his office or place of work or posted to the last known address and also to a conspicuous place in the Tribunal offices; or

|

| (c) |

publishing the particulars of the summons or notice in a newspaper circulating it in the area or any other media.

|

|

| (5) |

Every summons or notice issued under these Rules and requiring service shall be served by an officer of the Tribunal, a court process server, or any other person authorized to do so by the Tribunal including a police officer.

|

| (6) |

Any notice or summons served on an advocate, representative, or tax agent, of a party, by registered post or by leaving it at the chambers or office and whether it is for the personal appearance of the party or not, shall be presumed to be duly communicated and, unless the Tribunal otherwise directs, shall be effectual for all purposes as if it had been served on the party in person.

|

| (7) |

A summon, warrant, order, notice or other formal document issued by the Tribunal shall be signed by the Clerk, and shall be stamped with the stamp of the Tribunal.

|

|

| 17A. |

Warrant of arrest

Where, without sufficient cause, a witness fails to appear before the Tribunal when summoned, the Tribunal may on the proof that the witness was properly served with the summons, issue a warrant of arrest for the witness to be brought before the Tribunal on the date, time and place specified in the warrant. [L.N. 105/2016, r. 4.]

|

| 18. |

Consequences of non-attendance

| (1) |

When neither party attends on the day fixed for hearing, if satisfied that the notice of hearing was duly served to the parties, the Tribunal may dismiss the appeal or give such orders that it may deem appropriate.

|

| (2) |

Where only the appellant attends and if the Tribunal is satisfied that the notice of hearing was—

| (a) |

duly served, it may proceed ex parte;

|

| (b) |

not duly served, it shall direct a second notice to be served; or

|

| (c) |

not served in sufficient time or for other reasonable cause, the respondent was unable to attend, it shall postpone the hearing.

|

|

| (3) |

Where only the respondent attends and if the Tribunal is satisfied that notice of hearing was—

| (a) |

duly served, it may dismiss the appeal;

|

| (b) |

not duly served, it shall direct a second notice to be served; or

|

| (c) |

not served in sufficient time or for other reasonable cause, the appellant was unable to attend, it shall postpone the hearing.

|

|

|

| 19. |

Setting aside, varying or reviewing of decisions or dismissal

Upon an application by the applicant, the Tribunal, stating the reasons, may set aside, vary or review a decision made under these Rules.

|

| 20. |

Order of addresses

| (1) |

The Tribunal shall at the hearing of an appeal, hear the appellant and his witnesses first and the respondent shall be given an opportunity to cross examine the witness, if any.

|

| (2) |

Before the case is concluded, the evidence of the respondent shall be heard, and the appellant shall be given the opportunity to cross examine each witness followed by re-examination by the respondent after which the parties may make oral or written submissions.

|

| (3) |

The Tribunal may, at any time, put questions to either party or to any witness, and may, at its discretion, call additional evidence as it may be necessary for further clarification of the issues raised at the hearing of the appeal.

|

| (4) |

The Tribunal may, for sufficient reason, at any time after beginning the hearing of the appeal, adjourn the hearing; and in every such situation, the Tribunal shall fix another convenient day for further hearing.

|

|

| 21. |

Amendment of pleadings

A party may at any time before the closure of the case, orally apply to amend its pleadings and the Tribunal may, at its discretion, allow such application on such terms and conditions including granting leave to the other party to amend its pleadings provided the amendments do not raise new issues.

|

| 22. |

Recording of evidence

| (1) |

The evidence of the parties and that of a witness shall be recorded by the members of the Tribunal, or by a person authorized to do so, in a form to be decided upon by the members and when completed shall be signed by the members of the Tribunal at that proceeding.

|

| (2) |

Notwithstanding paragraph (1), the evidence given at the hearing of an appeal may be recorded in short hand or by mechanical means, and the transcript of anything recorded shall, if certified by members of the Tribunal at that proceeding to be correct, be deemed to be a true record of the evidence for the purposes of the proceeding.

|

|

| 23. |

Decision to be made in presence of parties

| (1) |

After concluding the hearing of the evidence and submissions of the parties, the Tribunal shall, as soon as practicable, make a written decision which shall, on notice to both parties, be read in their presence or of their advocates or representatives and shall cause a copy, duly signed by the members of the Tribunal which heard the appeal, to be served to each party to the proceeding.

|

| (2) |

The decision of the Tribunal shall be determined by a majority of the members present and voting at the meeting, and in the case of an equality of votes the chairperson shall have a casting vote in addition to his deliberative vote.

|

|

| 24. |

Contents of decision

The written decision of the Tribunal shall contain—

| (a) |

the nature of the appeal;

|

| (b) |

summary of the facts of the case;

|

| (c) |

the issues for determination citing the relevant tax law;

|

| (d) |

the arguments by the appellant and the respondent on the issues;

|

| (e) |

a summary of the relevant evidence produced before the Tribunal and the findings on each issue;

|

| (f) |

the relief or remedy, if any, to which the appellant or respondent is entitled; and

|

| (g) |

an order for costs or other relief.

|

|

| 25. |

Evidence by affidavit and interrogatories

| (1) |

Where the Tribunal requires evidence to be received by means of affidavits or interrogatories, the affidavits or interrogatories and the answers shall be by such means and in such form as the Tribunal may direct.

|

| (2) |

In any proceeding where the evidence of a witness who resides outside Kenya is necessary, the Tribunal may issue a commission or letter of request to examine that witness abroad.

|

| (3) |

A party may present its evidence to the Tribunal either orally, by affidavit, statement on oath or by combination of any of these methods.

|

|

| 26. |

Publication of decisions

The Secretary of the Tribunal shall within fourteen days from the date of making the decision, submit a copy of that decision to the Kenya Law Reports for publication. [L.N. 105/2016, r. 5.]

|

| 27. |

Tribunal to determine own procedure in certain matters

The Tribunal may determine an appropriate procedure where there are no applicable procedures under these Rules or the Act.

|

| 28. |

Revocation and saving

| (1) |

The following Rules are revoked—

| (a) |

the Income Tax (Local Committee) Rules, 1974 (L.N. No. 7/1974);

|

| (b) |

the Income Tax (Tribunal Rules) Rules, 1974 (L.N. No. 5/1974);

|

| (c) |

the Customs and Excise (Appeals) Rules, 2000 (L.N. No. 67/2000); and

|

| (d) |

the Value Added Tax (Appeals) Rules, 1990 (L.N. No. 229/1990).

|

|

| (2) |

Notwithstanding the provisions of paragraph (1)—

| (a) |

all things lawfully done under the repealed rules which are in force and effect immediately before the commencement of these rules including decisions or directions given under the repealed rules shall so far as consistent with these Rules and anything done under them continue to be in force and effect after the commencement; and

|

| (b) |

where any proceedings in respect of an appeal have been commenced before the date of commencement of these Rules, any step in the proceedings taken in accordance with the repealed Rules shall be deemed to have been validly taken for purposes of these Rules.

|

|

|

THE TAX APPEALS TRIBUNAL (PROCEDURE) RULES

| 1. |

Citation

These Rules may be cited as the Tax Appeals Tribunals (Procedure) Rules.

|

| 2. |

Interpretation

In these Rules, unless the context otherwise requires—

"Act" means the Tax Appeals Tribunals Act (Cap. 469A);

"appeal” has the meaning assigned to it under section 2 of the Act:

"appellant" means a person who has made an application to the Tribunal for review of a taxation decision under section 12, an extension of time under section 13(3) or reinstatement of an application under section 27(5);

"Chairperson" has the meaning assigned to it under section 2 of the Act;

“clerk" means a person appointed as such under section 11 of the Act;

“Commissioner's representative" means a person authorized to appear on behalf of the Commissioner before the Tribunal;

"officer in charge of registry" means a person appointed by the Secretary to be in charge of tax appeals registry;

"respondent" means a party against whom an appeal or an application is filed;

"Secretary" has the meaning assigned to it under section 2 of the Act;

"tax decision” means—

| (b) |

a determination of the amount of tax payable or that will become payable by a taxpayer;

|

| (c) |

a determination of the amount that a tax representative, appointed person, director or controlling member is liable for;

|

| (d) |

a decision on an application by a self-assessment taxpayer;

|

| (f) |

a decision requiring repayment of a refund; or

|

|

| 3. |

Form and Filing of appeal

| (1) |

A notice of appeal to the Tribunal shall be—

| (a) |

in Form TAT-1 set out in the Schedule; and

|

| (b) |

submitted electronically or physically to the clerk of the Tribunal within thirty days upon receipt of the decision by the Commissioner.

|

|

| (2) |

The appellant shall, within fourteen days from the date of filing the notice of appeal, submit enough copies, as may be advised by the clerk, of—

|

|

| 4. |

Memorandum of appeal

A memorandum of appeal referred in rule 3(2) shall—

| (a) |

be signed by the appellant;

|

| (b) |

set out concisely under distinct heads, numbered consecutively, the grounds of appeal without argument or narrative:

|

| (c) |

contain an index of all documents in the appeal with number of pages at which they appear; and

|

| (d) |

be accompanied by a copy of the—

|

|

| 5. |

Statement of facts of appellant